A Guide to Bond Ladders for Steady Income

Investing in bonds can often feel like a game of bad timing. If you buy a long-term bond that locks your money up for ten years, you might deeply regret it if interest rates spike next year. On the flip side, if you only buy short-term bonds to keep your money safe, you will usually miss out on the higher payouts that long-term investments offer.

A bond ladder is a classic financial strategy designed to solve this exact dilemma. It allows you to enjoy the higher payouts of long-term bonds while still giving you regular access to your cash.

What is a Bond Ladder?

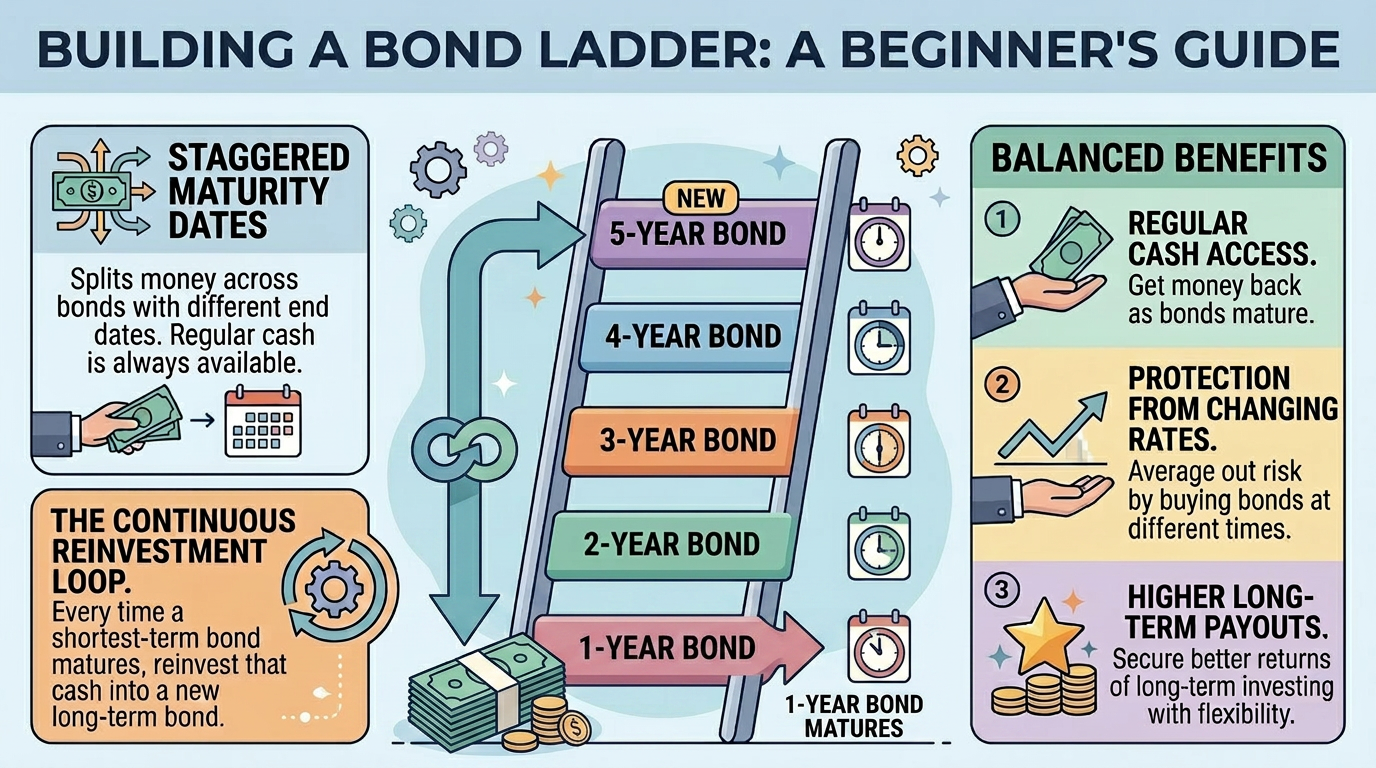

A bond ladder is a portfolio of bonds that mature at staggered intervals over time. Instead of putting all your cash into a single bond that pays you back on one specific date, you spread your money across several different bonds that finish at different times.

Think of each bond maturity date as a rung on a ladder. By spacing these rungs out evenly, you ensure that your money is never completely locked up all at once.

How a Bond Ladder Works in Real Life

To see how this strategy operates, imagine you have $50,000 that you want to invest in fixed-income assets. Instead of buying one giant $50,000 bond, you decide to build a five-year ladder.

You divide your money into five equal pieces of $10,000 and buy five separate bonds:

Rung 1: A $10,000 bond that matures in 1 year.

Rung 2: A $10,000 bond that matures in 2 years.

Rung 3: A $10,000 bond that matures in 3 years.

Rung 4: A $10,000 bond that matures in 4 years.

Rung 5: A $10,000 bond that matures in 5 years.

When the first year ends, your one-year bond matures. The issuer pays you back your initial $10,000 plus the interest you earned.

Now comes the trick that keeps the ladder going. You take that $10,000 and reinvest it into a brand-new five-year bond. Because your other original bonds have now aged by a year, your portfolio still has bonds that will mature in one, two, three, four, and five years. You have created a continuous loop where cash frees up automatically every single year.

The Major Benefits of the Ladder Strategy

Building a bond ladder offers three massive advantages for everyday investors who want to protect their savings.

Flexibility and Liquidity: Liquidity is just a financial term for how quickly you can turn an investment back into cash. If you experience an emergency, you know you have a chunk of money becoming available at the end of the year without having to sell an investment early for a penalty.

Protection Against Interest Rates: If interest rates rise across the economy, you are not trapped in low-paying investments. Because you have cash freeing up every year, you can constantly reinvest that money into new bonds at the current higher rates.

Higher Overall Yields: Short-term bonds typically pay very little interest. By continuously rolling your maturing funds into new long-term bonds at the top of your ladder, you eventually earn the higher interest rates of long-term bonds while maintaining the safety of a short-term timeline.

Summary

A bond ladder is a smart, predictable way to invest in fixed income without gambling on where interest rates are going. By splitting your money across bonds that mature at staggered intervals, you create a self-sustaining loop of steady cash flow. It gives you the best of both worlds: the high returns of long-term investing and the peace of mind that comes with regular liquidity.