The Big Three Bonds: Treasury, Municipal, and Corporate

When you decide to invest in bonds, you will quickly learn that who you lend your money to matters immensely. While all bonds are fundamentally loans, the borrower dictates the risk of the loan, the amount of interest you will earn, and how your earnings will be taxed. To truly understand the bond market, you must look beyond the basics and dive into the specific features of the three main types of bonds: Treasury, municipal, and corporate.

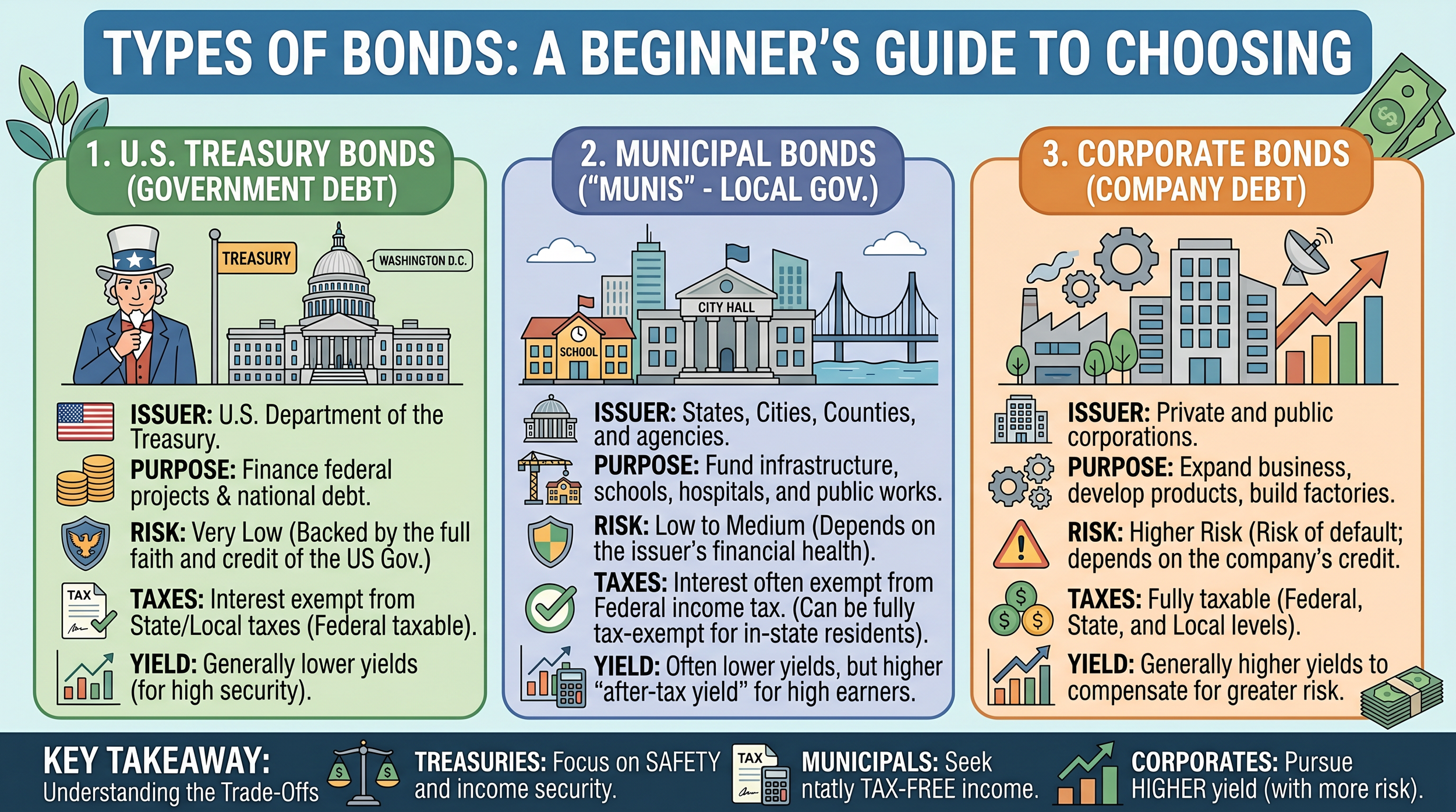

Treasury Bonds: The Safest Bet and Its Variations

Treasury bonds are loans you make to the U.S. federal government. Because the U.S. government backs them, they are considered the safest investment you can make, with the chance of default, which occurs when a borrower fails to make scheduled interest payments or cannot pay back the original loan amount, being practically zero. However, this absolute safety means you earn less money, as lower risk usually equals lower returns. For taxes, you must pay federal tax on the interest you earn, but you do not pay state or local taxes, making them excellent if you live in a high-tax state. It is important to know that Treasuries come in different lengths, formally called maturities. Treasury Bills mature in one year or less, Treasury Notes mature in two to ten years, and Treasury Bonds mature in twenty to thirty years. Additionally, the government offers Treasury Inflation-Protected Securities, known as TIPS, which automatically adjust their principal value to keep pace with inflation, ensuring your money does not lose its purchasing power over time.

Municipal Bonds: Local Projects, Tax Savings, and Revenue Streams

Municipal bonds, or "munis," are loans to states, cities, or counties to help pay for public projects like schools, highways, or hospitals. These bonds are slightly riskier than Treasury bonds but still very safe, though there is a small chance a local government could face financial trouble. The best part about municipal bonds is the tax savings, as the interest you earn is usually entirely free from federal taxes. If you buy a bond from your home state or city, your earnings are often free from state and local taxes as well. Within municipal bonds, there are two main types you should understand. General Obligation bonds are backed by the full taxing power of the municipality, making them incredibly secure. Revenue bonds, on the other hand, are backed only by the income generated from the specific project they fund, such as toll roads or utility water bills, making them slightly riskier if the project fails to generate the expected income.

Corporate Bonds: Ratings, Risk, and Higher Rewards

Corporate bonds are loans made to companies so they can grow, build factories, or buy equipment. Unlike governments, a company cannot simply raise taxes to pay off its debts, meaning if a business fails, it might not pay you back. To compensate for this elevated risk, companies pay a higher interest rate. Keep in mind that the interest you make on corporate bonds is fully taxed by both the federal and state governments. Because every company is different, independent financial agencies assign credit ratings (ratings on the credit of a company) to corporate bonds to help investors easily understand the risk. Companies with rock-solid finances receive an Investment Grade rating, meaning they are highly likely to pay you back. Companies with shakier finances receive lower ratings, often called High-Yield or Junk Bonds, which pay incredibly high interest rates to attract investors but carry a significant, real risk of default.

How to Buy and Manage Your Bonds

Now that you know the types of bonds and their specific quirks, you need to know how to acquire them. The most direct way to buy Treasury bonds is through the government's official website, TreasuryDirect, where you can purchase them directly without paying any middleman fees. For corporate and municipal bonds, you will typically need to use a standard brokerage account. However, buying individual corporate or municipal bonds can be expensive and requires a lot of intensive research. Because of this, most beginner and intermediate investors choose to buy bond Mutual Funds or Exchange-Traded Funds (ETFs). These funds pool your money with thousands of other investors to buy massive, diversified baskets of bonds. By purchasing a single share of a bond ETF, you instantly own tiny pieces of hundreds of different bonds, which drastically lowers your risk and makes managing your investments incredibly simple.

Balancing Your Portfolio for the Long Term

It is important to remember that bonds are usually just one piece of a broader investment puzzle. A well-rounded portfolio typically includes a mix of different assets, such as stocks for long-term growth or real estate, with bonds serving as the stabilizing anchor. When deciding on the bond portion of your overall portfolio, choosing the right mix depends entirely on your personal financial goals and timeline. If your main objective is keeping your cash completely safe from market crashes, Treasury bonds are your best foundation. If you are in your peak earning years and want to shield your investment income from the IRS, municipal bonds are a highly effective tool. If you want to maximize the interest you earn and can tolerate minor fluctuations in your account value, adding high-quality corporate bonds will boost your overall returns. By combining these three bond categories alongside your other investments, you can build a robust, customized portfolio that provides steady income and peace of mind, perfectly balancing out your riskier assets regardless of what the stock market is doing.

Summary

To wrap up, bonds are essentially loans you make to different organizations in exchange for regular interest payments. Treasury bonds offer unmatched safety backed by the U.S. government but come with lower returns. Municipal bonds help fund local projects and provide excellent tax advantages, making them ideal for investors in higher tax brackets. Corporate bonds fund business growth and offer the highest potential interest rates, but they carry a higher risk of default that requires careful attention to credit ratings. By understanding these three main categories and utilizing tools like bond funds or ETFs for easy diversification, you can confidently build a well-rounded portfolio. Whether you prioritize absolute security, tax-free income, or higher yields, the bond market has a specific tool designed to help you manage risk and reach your long-term financial goals.