Market Summary (May 25- May 29, 2026)

Market Summary

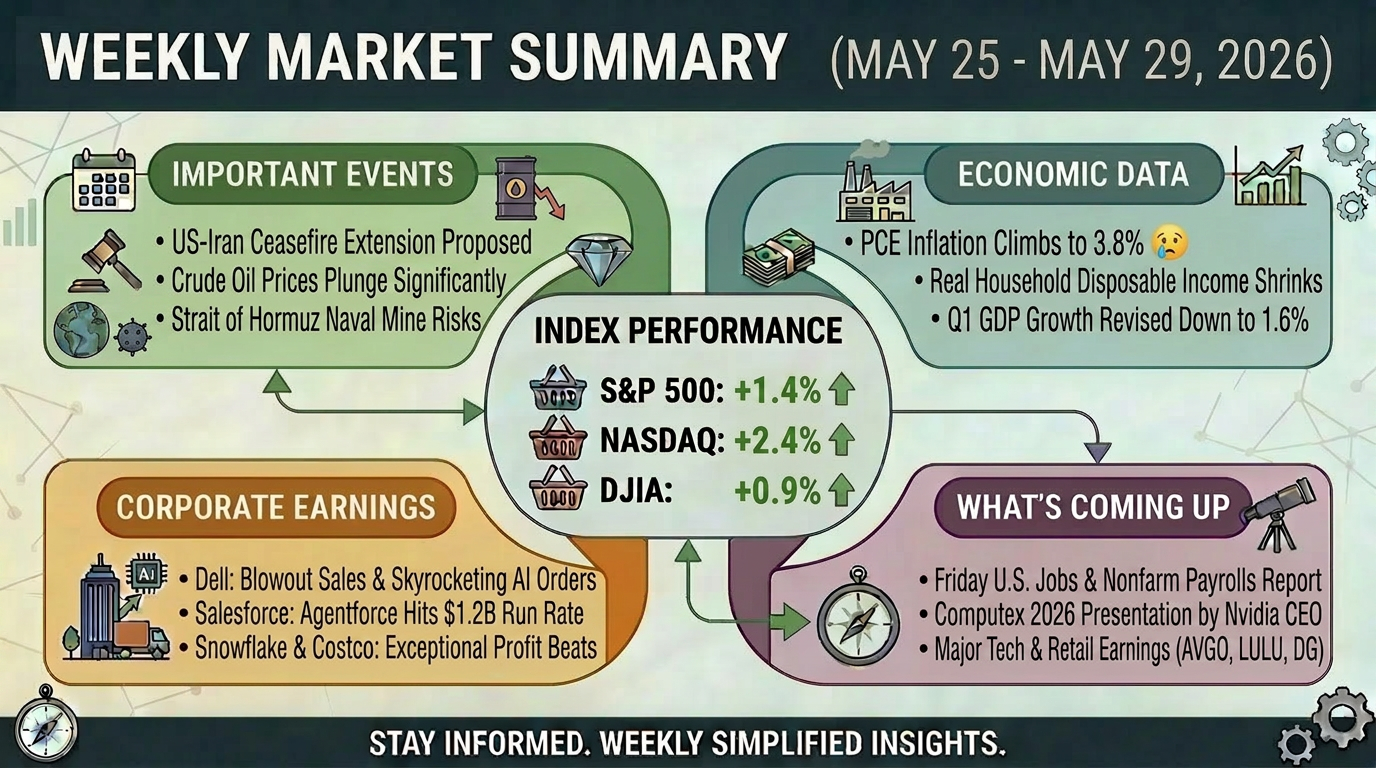

Wall Street shrugged off earlier anxieties to stage a spectacular rally, pushing major stock indexes to new heights. Leading the charge, the S&P 500 logged its ninth consecutive positive week (marking its most prolonged weekly winning streak since 2023) by gaining 1.4% to finish at a record-breaking 7,580.06. The tech-heavy Nasdaq Composite outperformed its peers with a powerful 2.4% weekly jump to close at 26,972.62, while the Dow Jones Industrial Average notched a modest 0.9% increase to land at 51,032.46. Beneath this broad success, a sharp division remained visible. The technology sector alone surged by over 15.0% during May, leaving the majority of non-tech sectors behind as investors favored very specific, high-growth names.

Important Events

A welcome wave of diplomatic progress in the Middle East served as the primary driver for the market's optimistic mood. Investors breathed a sigh of relief on news of a proposed 60-day ceasefire extension between Iran and the United States. Even though the agreement still awaits a formal sign-off from President Trump, energy markets immediately relaxed. West Texas Intermediate (WTI) crude oil shed 1.5% on Friday to settle at $87.55 per barrel, completing a steep weekly decline of roughly 10.0%. Similarly, Brent crude pulled back by 1.7% to end at $91.38 per barrel, which is a significant retreat from its recent conflict-driven high of $112.

However, underlying dangers persist; U.S. intelligence confirmed that at least 10 naval mines are still drifting in the vital Strait of Hormuz shipping corridor. Additionally, a new diplomatic dispute is brewing over Iran's proposal to set up a maritime payment network with Oman for "transit charges" to bypass international shipping rules, an idea that U.S. Secretary of State Marco Rubio firmly dismissed.

Economic Data

Even as financial markets cheered, the latest economic reports painted a much tougher picture for everyday Americans. The government's April Personal Consumption Expenditures (PCE) report revealed that headline inflation climbed to 3.8% year-over-year from 3.5% in March, hitting its highest annual rate since mid-2023. Core inflation, which excludes unpredictable food and energy costs, edged up to 3.3% annually, staying well above the Federal Reserve's 2.0% comfort zone despite a mild 0.2% monthly gain that was slightly lower than expected.

With prices climbing faster than flat wages, household spending power eroded quickly. Real after-tax disposable income dropped by 0.5% in April, leading to a 1.1% decline compared to last year. Outside of unusual pandemic shifts, this represents the worst annual drop in household income since the Great Recession in 2009, forcing families to exhaust their personal savings. Furthermore, economic growth is losing steam, with first-quarter GDP revised downward to an annualized 1.6% from the prior 2.0% estimate. On a positive note, falling oil prices helped lower borrowing costs. The 10-year U.S. Treasury yield cooled to 4.5% and the policy-sensitive 2-year yield dipped to 4.0%, which provided fresh liquidity to growth companies and lifted gold prices to a record $4,556.98 per ounce.

Corporate Earnings

Dell Technologies: Dell posted stunning first-quarter results that completely re-energized the tech sector. Fueled by a massive 757.0% yearly explosion in AI-optimized server sales to $16.1 billion, total revenue surged 88.0% over last year to reach $43.8 billion. Profits easily surpassed Wall Street forecasts, and executive leadership boosted their full-year sales projections, triggering a spectacular 32.8% single-day stock surge on Friday.

Salesforce: The cloud software pioneer reported a healthy 13.3% revenue expansion to $11.1 billion. In a first-of-its-kind financial disclosure, the company revealed that its brand-new agentic AI platform, Agentforce, has already built a $1.2 billion run rate in recurring revenue. Despite some initial investor worry over softer marketing software trends, the stock bounced back aggressively on Friday with a 4.2% gain.

Snowflake: Snowflake enjoyed a massive operational turnaround, posting a 33.0% increase in top-line revenue to $1.39 billion while beating earnings estimates by a staggering 178.6%. The company is capitalizing on corporate clients moving massive datasets onto its system to train proprietary AI tools, driving the stock to a phenomenal 36.0% weekly gain.

Costco Wholesale: Demonstrating why wholesale clubs excel when inflation pinches wallets, Costco saw its total revenue rise 11.6% to $70.5 billion. Customer loyalty remained exceptionally firm, highlighted by a 92.2% membership renewal rate in the U.S. and Canada. Total net income expanded by 15.2%, keeping the stock trading near its all-time high of $1,005 per share.

What’s Coming Up Next Week

Heading into the first week of June, global markets will turn their attention to vital labor data and high-profile artificial intelligence developments. The main economic highlight arrives on Friday with the U.S. Jobs Report, where forecasters anticipate a solid addition of 100,000 positions and a steady unemployment rate of 4.3%. Ahead of that, fresh data on manufacturing and services activity will offer the Federal Reserve final clues before its monetary policy meeting in mid-June. In the tech arena, global attention shifts to the Computex 2026 event in Taipei, where Nvidia chief Jensen Huang will host a highly anticipated presentation. Analysts will parse his introduction of the next-generation "Vera" and "Rubin" chip designs to determine if corporate AI infrastructure spending can maintain its current momentum.

A heavy slate of high-profile corporate earnings will also test market sentiment:

Broadcom (AVGO) reports on Wednesday, serving as a direct gauge for advanced networking and custom chip demand following Dell's massive week.

Hewlett Packard Enterprise (HPE) delivers results on Monday, which will show whether the booming demand for AI servers is spreading across the entire tech sector or limited to specific companies.

Palo Alto Networks (PANW) and CrowdStrike (CRWD) will report mid-week, revealing whether the rush to buy AI hardware is creating a parallel wave of investment in data security.

Dollar General (DG) and Lululemon (LULU) drop results on Tuesday and Thursday respectively, giving investors an excellent look at the fragmented consumer landscape by contrasting discount grocery trends with high-end retail demand.