A Simple Guide to Credit Ratings, Financial Report Cards

If you have ever applied for a credit card, a car loan, or a mortgage, you already know about consumer credit scores. A three-digit number dictates how trustworthy you are to lenders and determines the interest rate you will pay.

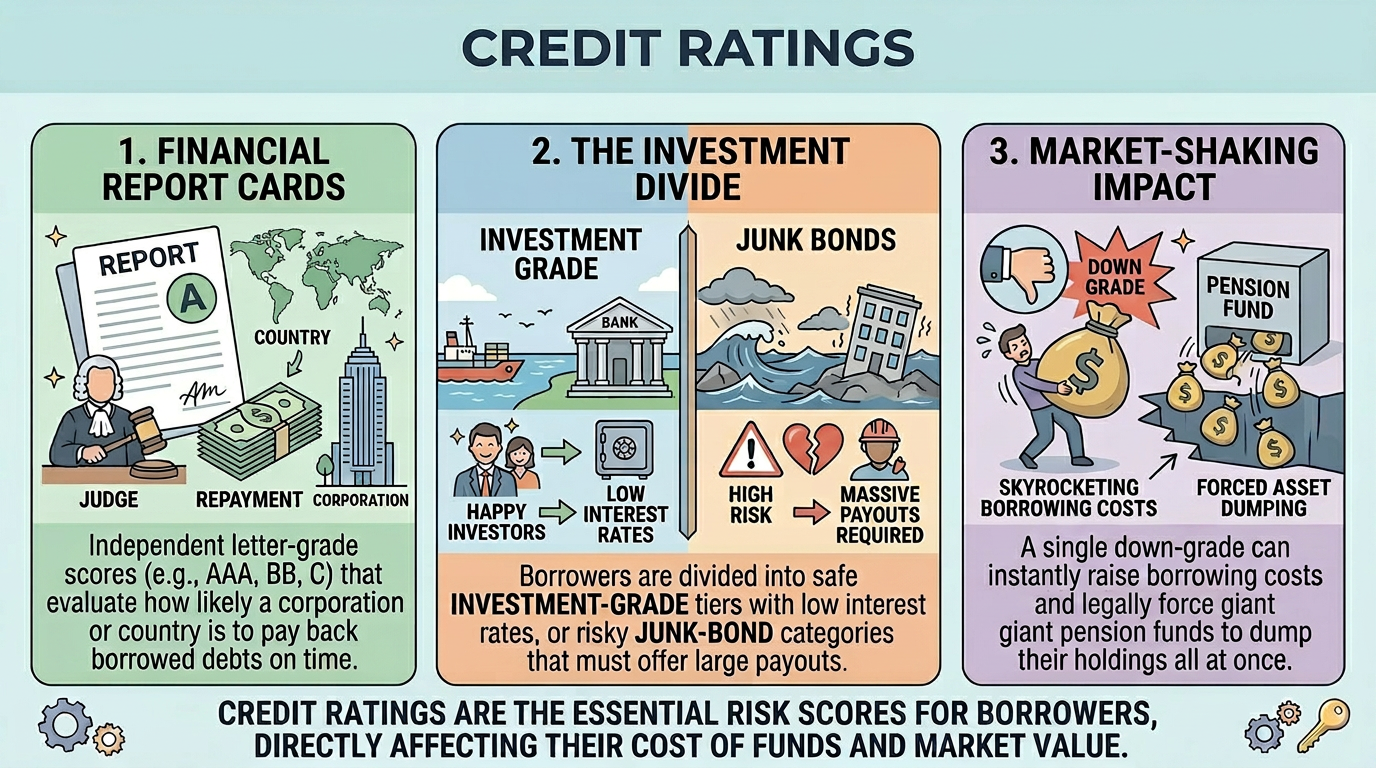

The exact same report card system exists for massive corporations and entire countries. Instead of a three-digit score, these giant entities are assigned credit ratings. These ratings are the financial world's shorthand for risk, and a single upgrade or downgrade can instantly redirect the flow of billions of dollars across the global economy.

What is a Credit Rating?

A credit rating is an independent evaluation of a borrower's ability to pay back their debts on time. It acts as an official stamp of financial health.

When a giant tech company or a foreign government wants to borrow money, they issue bonds to investors. Before investors hand over their hard-earned cash, they want to know the likelihood of getting paid back. Credit ratings provide that answer.

Three massive independent companies dominate this space. They are S&P Global Ratings, Moody's Investors Service, and Fitch Ratings. These firms employ armies of analysts to dig through financial statements, economic data, and political stability to issue a letter-grade score.

The Letter Grade System

The rating agencies use a standardized alphabet soup of grades to rank financial reliability. While the specific lettering varies slightly between agencies, they generally follow a familiar pattern:

AAA (Triple-A): This is the gold standard. It represents the highest possible rating and means the borrower has an incredibly stable capacity to meet its financial commitments.

AA and A: These are highly secure, upper-medium-grade ratings indicating very low risk, though they are slightly more vulnerable to economic downturns than Triple-A entities.

BBB: This represents the lowest tier of adequate financial health. The borrower is currently stable but could face trouble if economic conditions deteriorate significantly.

BB, B, CCC, and CC: These are speculative grades. Borrowers in this territory face significant ongoing uncertainties and possess real default risks.

D: This stands for default. The borrower has failed to pay back its obligations on time.

The Great Divide: Investment Grade vs. Junk Bonds

The most critical concept in the credit rating world is the boundary line between two major categories: investment grade and speculative grade. Speculative grade assets are also famously known as junk bonds or high-yield bonds.

The line is drawn right below the BBB tier. Anything rated triple-B or higher is considered investment grade. These are safe, dependable investments issued by stable companies and reliable governments. Because the risk of default is so low, these borrowers get to pay very low interest rates to their investors.

Anything rated double-B or lower falls into the junk bond category. These issuers are financially shaky or dealing with heavy debt burdens. To convince anyone to lend them money, they have to pay incredibly high interest rates. This is why junk bonds are attractive to aggressive investors who are willing to take on massive default risks in exchange for huge payouts.

Why Credit Ratings Shake the Global Economy

Credit ratings are much more than just informational tools. They carry serious real-world consequences for the entire financial system.

First, they dictate borrowing costs. If a major company suffers a credit downgrade from investment grade to junk status, its borrowing costs skyrocket overnight. They must immediately start paying higher interest rates on all new debt, which eats into their profits and can stunt their business growth.

Second, they trigger automatic sell-offs. Many massive institutional investors, such as multi-billion-dollar pension funds and university endowments, operate under strict legal mandates. Their bylaws often state that they are only allowed to hold investment-grade assets. If a government or a giant blue-chip corporation gets downgraded into the speculative tier, these giant funds are legally forced to dump millions of shares or bonds all at once, causing panic and price crashes in the open market.

Summary

Credit ratings are essential financial report cards that evaluate how likely a corporation or a country is to default on its debts. By sorting borrowers into clear categories from elite investment grade down to risky junk bonds, the major rating agencies create a universal language of risk. A simple change in these letter grades can instantly change a borrower's interest rates, shift institutional portfolios, and alter the stability of the global economy.