How Interest Works Against You: The Psychology of APR

Credit cards are designed to be incredibly convenient, but they also use clever psychological tricks to keep you in debt. When you carry a balance from month to month, credit card companies put the math of interest to work against you. While you focus on the seemingly affordable monthly minimum payment, interest is silently multiplying in the background. To avoid falling into a permanent debt trap, you need to understand exactly how credit card interest works, how it keeps your balance high, and the hidden cost of buying things on credit.

Breaking Down APR and Compounding Interest

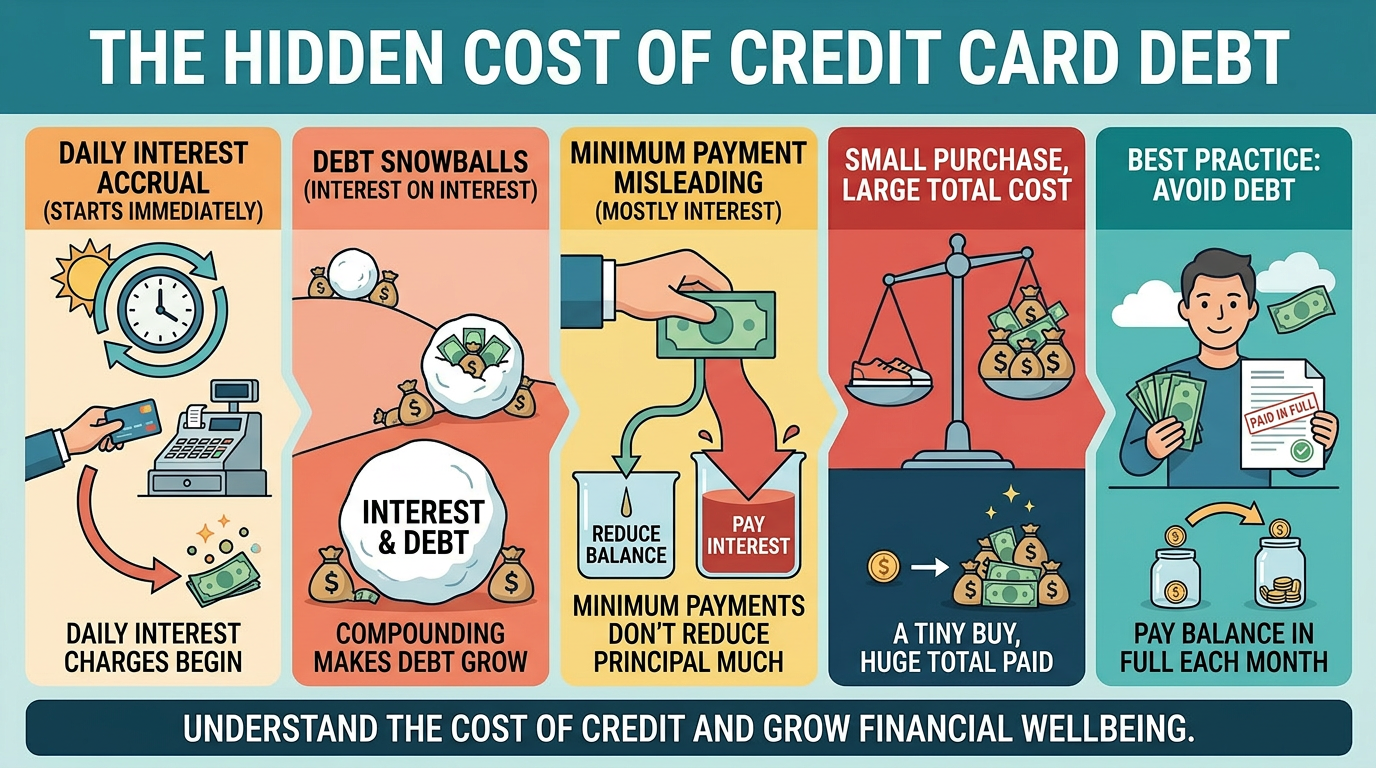

When you look at a credit card offer, the most prominent number you see is the Annual Percentage Rate or APR. This is the yearly interest rate you are charged for borrowing money on the card. However, the term annual is highly misleading. Credit card companies do not calculate your interest once a year. Instead, they divide your APR by 365 to find your daily interest rate, and then they charge you based on your average balance every single day.

This daily calculation triggers a dangerous cycle known as compounding interest, which means the bank charges you interest on your original balance plus all the previous interest you have already accumulated. If you do not pay your balance in full, your debt grows larger every day, and you end up paying interest on your interest. This math creates a snowball effect that works in favor of the bank, making your debt heavier and harder to clear the longer you leave it unpaid.

The Trap of the Minimum Payment

Credit card companies are legally required to show you a minimum payment on your monthly statement, which is usually around two to three percent of your total balance. Psychologically, this number acts as a relief. It makes a large debt feel completely manageable, giving you the false impression that you are handling your finances well. In reality, the minimum payment is a trap designed to keep you in debt for as long as possible.

Your total credit card debt is made up of two parts: the interest fees and the principal balance, which is the actual amount of money you originally spent on purchases. When you make only the minimum payment, the bank takes its interest fees out of that money first, leaving only a tiny sliver of cash to pay down the actual principal balance. Because the principal barely drops, the bank can charge you almost the exact same amount of interest again the very next month, keeping you stuck on a financial treadmill.

The True Cost of a Retail Purchase

To see how this works in real life, consider the true cost of using a credit card for a common retail purchase without paying it off right away. Imagine you buy a one thousand dollar television using a credit card with a typical twenty-two percent APR. If you decide to only pay the minimum payment every month, you might assume you will eventually pay a little more than one thousand dollars over time.

The mathematical reality is shocking. By paying only the minimum, it will take you nearly ten years to fully pay off that television. Furthermore, over those ten years, you will pay over one thousand two hundred dollars just in interest fees on top of the original price. That one thousand dollar television ends up costing you more than two thousand two hundred dollars. By the time you finally finish paying for it, the television will likely be broken or completely outdated.

Summary

Credit card companies maximize their profits by exploiting human psychology through low minimum payments and hidden daily interest. By understanding that your APR creates daily compounding interest, you can see how easily a small balance can spiral out of control. Minimum payments are mathematically designed to cover interest fees while barely touching your principal balance, dragging out your debt for years. To protect your wallet, you must look past the illusion of low monthly payments and recognize that carrying a balance turns everyday retail purchases into incredibly expensive, long-term financial burdens.