A Guide to Debt Timing and Prioritization

Finding extra money in your budget is an exciting milestone, but it immediately introduces a difficult financial riddle. Should you use that extra cash to pay off your debt as fast as possible, or should you put it into a savings account or the stock market? Many people assume that all debt is an emergency that must be wiped out immediately. However, rushing to pay off debt without a clear strategy can actually leave you vulnerable to financial emergencies or cause you to miss out on building long-term wealth. To make the best choice, you need to understand the right timing and order of operations for managing your liabilities.

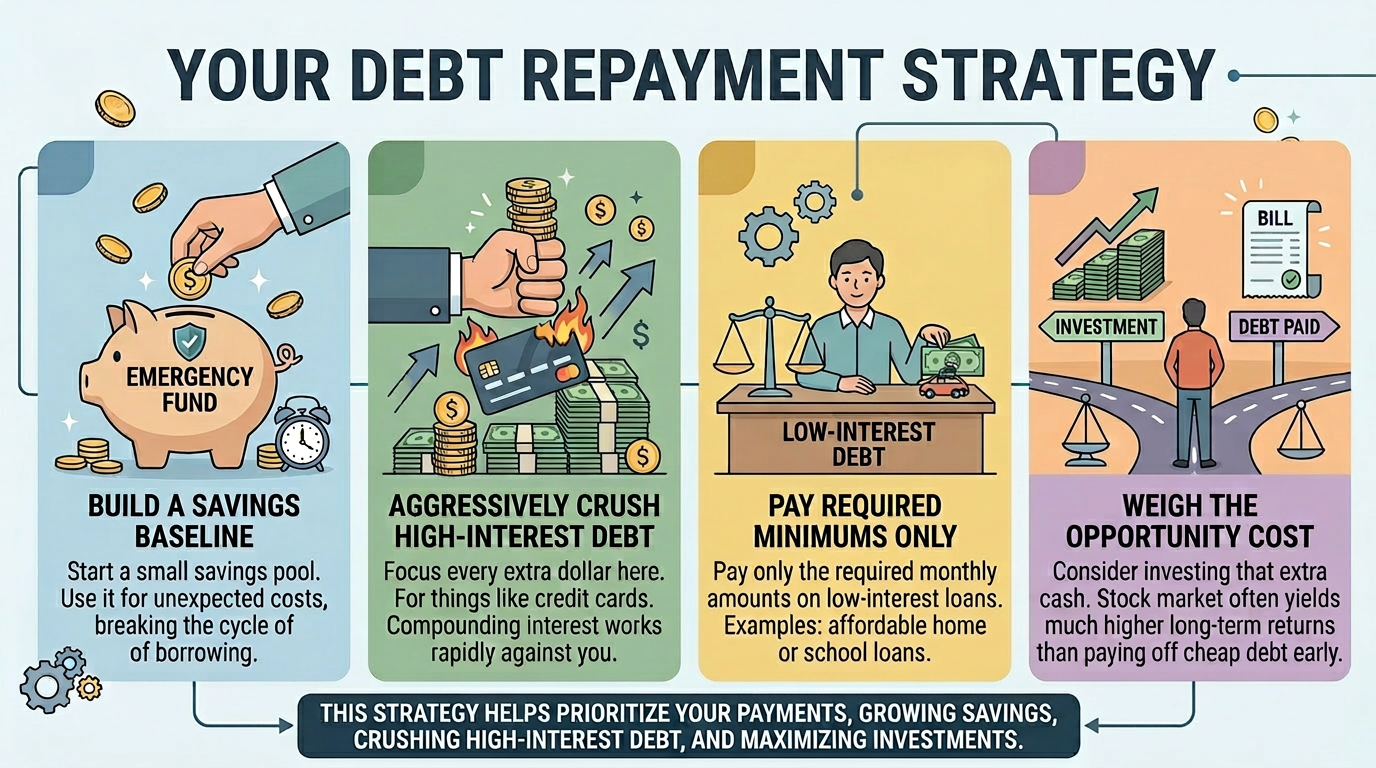

Secure Your Emergency Baseline First

The biggest mistake you can make is throwing every spare dollar at your debt when you have zero dollars saved in the bank. If you do this, the next unexpected expense, such as a car repair or a medical bill, will instantly force you to borrow money again, trapping you in a toxic cycle. Before you pay even one extra dollar toward your debt principal, you must establish a starter emergency fund. This is a small savings cushion, usually between one thousand dollars and one month of basic living expenses, kept in a safe and accessible account. This baseline protection ensures that you can handle life's minor disruptions without adding to your total debt balance.

The Core Rule: Analyze the Interest Rate

Once your starter savings cushion is secure, the timing of your debt payoff depends entirely on how expensive your loans are. You can determine your strategy by categorizing your balances based on their annual percentage rates. A high-interest debt is any loan with an interest rate higher than what you could reliably earn by investing your money elsewhere, typically around seven percent or higher. Examples include credit cards, personal loans, and high-rate auto loans. This type of debt is a financial emergency because the interest compounds rapidly against you. You should attack high-interest loans aggressively with every extra dollar you can find.

Conversely, a low-interest debt is a loan with an interest rate well below that seven percent threshold, such as a modest mortgage or certain federal student loans. Because these loans cost you very little over time, paying them off ahead of schedule is not an emergency. You should maintain the minimum monthly payments on low-interest loans while redirecting your extra cash toward more productive financial goals.

Paying Off Debt versus Investing

When you are trying to decide whether to clear a low-interest loan early or invest that extra money in the stock market, you must consider the trade-offs. This decision requires you to weigh the opportunity cost, which is the financial loss of a potential gain from one option when you choose a different alternative. For example, if you use extra cash to pay off a mortgage with a three percent interest rate, your guaranteed return on that money is exactly three percent.

However, if you instead invest that extra cash in a diversified index fund that historically earns an average annual return of eight percent, your opportunity cost of paying down the mortgage early is the five percent difference you missed out on earning. When the numbers are in your favor, investing your extra cash is often the smarter mathematical choice for building long-term wealth.

Summary

Deciding when to pay off debt requires balancing immediate security with mathematical efficiency. You should never pay off debt aggressively until you have established a basic emergency fund to break the cycle of borrowing. Once your savings baseline is secure, prioritize your debt based on interest rates by attacking high-interest debt immediately while paying only the minimums on low-interest debt. By respecting the opportunity cost of your money, you can avoid the trap of rushing to clear cheap loans, allowing your extra cash to be invested where it can grow and build true financial freedom.