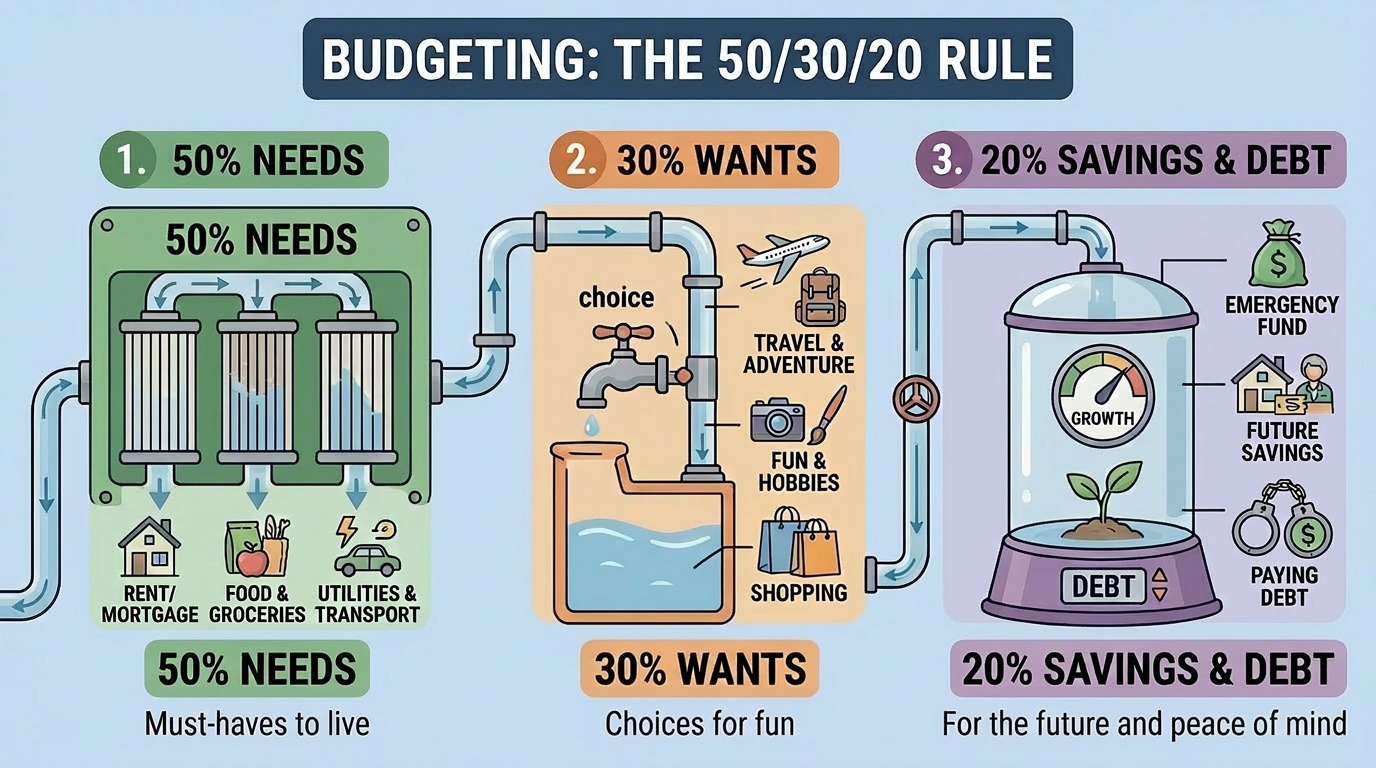

50/30/20, The Golden Rule For Budgeting

Managing money can feel overwhelming, especially with endless advice demanding that you track every single penny. For those who want a clear and straightforward way to handle their finances without complicated spreadsheets, the 50/30/20 rule is a highly effective solution. Popularized by Senator Elizabeth Warren in her book "All Your Worth," this budgeting framework breaks your after-tax income into three simple categories.

50%: Needs

Half of your income should go toward your essential living expenses. These are the bills that absolutely must be paid for you to survive and maintain your basic quality of life. If you lost your job tomorrow, these are the expenses you would still have to cover.

Housing: Rent or mortgage payments.

Utilities: Electricity, water, heat, and basic internet.

Food: Essential groceries (this does not include dining out).

Transportation: Car payments, gas, insurance, or public transit passes.

Financial Obligations: Minimum payments on credit cards or student loans, child care, and health insurance.

If your essential needs take up more than 50% of your take-home pay, you might need to look for ways to reduce your fixed costs, such as moving to a cheaper apartment, or find ways to increase your overall income. On the other hand, if you have a high income, your essential living expenses might naturally fall well below that 50% mark. You certainly do not need to inflate your lifestyle to hit that number. Any leftover money in this category can simply be redirected toward your savings and debt payoff goals.

30%: Wants

This category is for the things that make life enjoyable but are not strictly necessary to survive. While traditional budgets advise against spending money on fun, the 50/30/20 rule builds it directly into your financial plan.

Dining Out: Restaurants, coffee shops, and delivery services.

Entertainment: Movie tickets, sporting events, hobbies, and streaming subscriptions.

Lifestyle Upgrades: The newest smartphone, trendy clothing, or a nicer car than you strictly need to get to work.

Travel: Vacations and weekend getaways.

Keeping this category at or below 30% ensures you can enjoy your hard-earned money without sabotaging your financial future.

20%: Savings and Debt Payoff

The final piece of the puzzle is dedicated to securing your financial future. This 20% goes toward building wealth, protecting yourself from emergencies, and eliminating financial burdens.

Emergency Fund: Saving cash in a highly accessible account for unexpected events like a medical bill or a sudden home repair.

Retirement and Investing: Contributing to a 401(k), an IRA, or other long-term investment accounts.

Extra Debt Payments: Any money put toward credit cards or student loans that goes above the required monthly minimum payment.

Consistently putting 20% of your income into this category is the secret to building long-term wealth and eventually achieving financial independence.

Why the 50/30/20 Rule Works

The brilliance of this system is its sheer simplicity. You do not have to track every individual receipt or feel guilty about buying a cup of coffee. As long as your overall spending fits into these three broad buckets, your finances will remain balanced. It provides enough structure to ensure your bills are paid and your future is funded, while still offering the flexibility to enjoy your life today.

Summary

The 50/30/20 rule is a straightforward but powerful way to manage personal finances. By dedicating 50% of your after-tax income to essential needs, 30% to personal wants, and 20% to savings and extra debt reduction, you create a perfectly balanced financial life. This method removes the stress of micro-managing your bank account and provides a clear, actionable roadmap to financial stability.