A Simple Guide to Creating Your Own Budgeting Plan

Many people hear the word "budget" and immediately think of strict rules and financial restrictions. However, a budget is simply a plan for your money. It tells your cash where to go instead of leaving you wondering where it went. While frameworks like the 50/30/20 rule are great starting points, the most successful budget is one you custom-build to fit your unique lifestyle and goals.

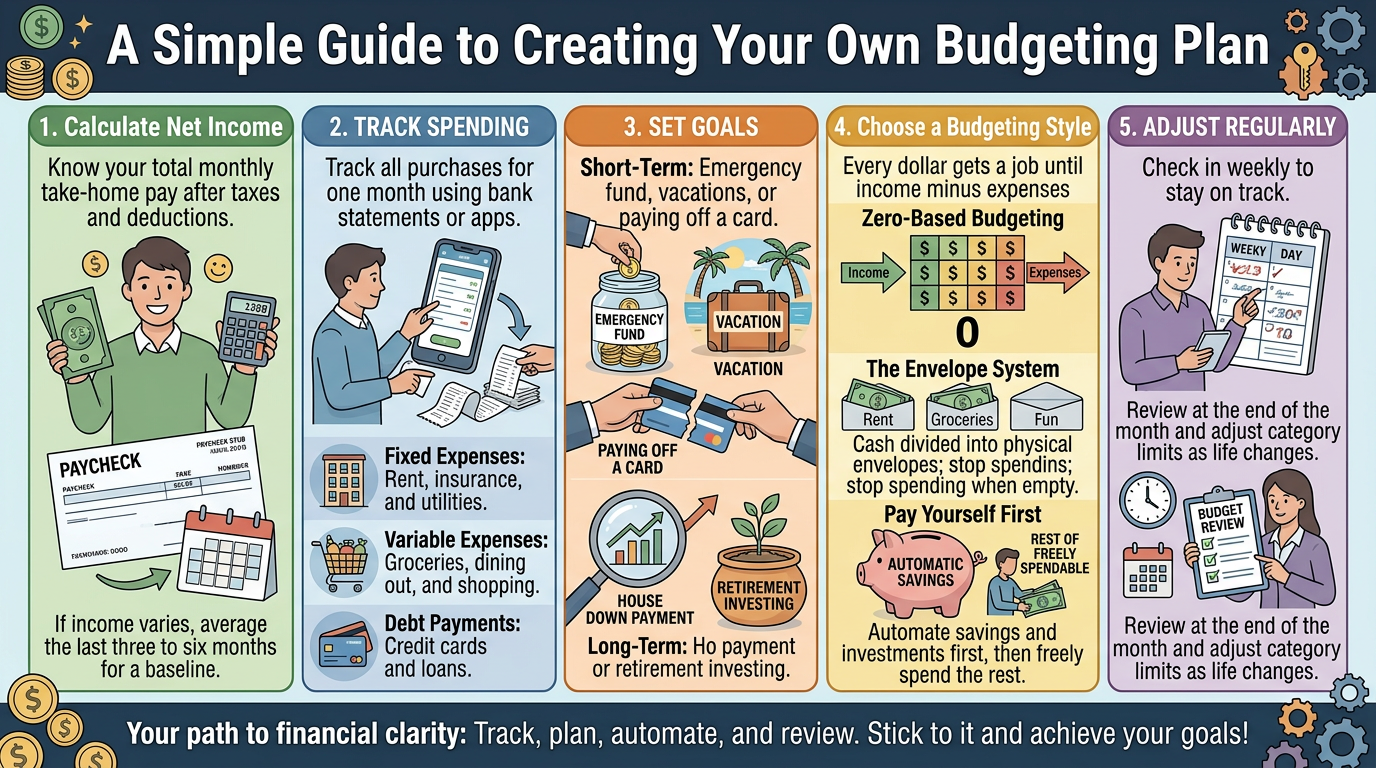

Here is a step-by-step guide to creating a personalized budgeting plan that actually works for you.

Step 1: Calculate Your Net Income

Before you can plan how to spend your money, you need to know exactly how much you have. Focus on your net income, which is your take-home pay after taxes, insurance, and any automatic retirement contributions are deducted.

If you have a steady salary, this number is easy to find on your pay stub. If you are a freelancer or work irregular hours, calculate your average monthly income based on the last three to six months to give yourself a realistic baseline.

Step 2: Track Your Current Spending

You cannot change your financial habits until you know what they are. Spend a month tracking every single purchase you make. You can do this by reviewing your bank statements, using a budgeting app, or carrying a small notebook.

Categorize your spending into clear buckets:

Fixed Expenses: Rent, car payments, insurance, and utilities. These stay mostly the same every month.

Variable Expenses: Groceries, dining out, entertainment, and shopping. These fluctuate and are the easiest places to cut back.

Debt Payments: Credit cards, student loans, or personal loans.

Step 3: Set Clear Financial Goals

A budget without a goal is hard to stick to. Ask yourself what you want your money to achieve in the short term and the long term.

Short-Term Goals: Building a small emergency fund, saving for a vacation, or paying off a specific credit card.

Long-Term Goals: Saving for a down payment on a house, aggressively investing for early retirement, or funding a child's education.

Writing these goals down gives your budget a purpose. When you are tempted to overspend, you can remind yourself of what you are actually working toward.

Step 4: Choose Your Budgeting Style

There is no single correct way to budget. Pick a framework that matches your personality:

Zero-Based Budgeting: Every single dollar is assigned a specific job before the month begins. Your income minus your expenses, savings, and investments should equal zero. This is great for detail-oriented people.

The Envelope System: You withdraw your spending money in cash and divide it into physical envelopes labeled for groceries, gas, and fun. When an envelope is empty, you stop spending in that category. This is highly effective for curbing impulse purchases.

Pay Yourself First: You immediately transfer money to your savings and investment accounts as soon as you get paid. You are then free to spend whatever is left over however you like.

Step 5: Monitor and Adjust Regularly

A budget is a living document, and it should change as your life changes. Your expenses will shift, your income will grow, and your priorities will evolve.

Sit down once a week for a quick five-minute check-in to make sure you are staying on track. At the end of every month, review what worked and what did not. If you constantly overspend in your grocery category, you may need to increase that budget and cut back somewhere else. The goal is progress, not perfection.

Summary

Building your own budgeting plan puts you in the driver's seat of your financial life. By understanding exactly what you earn, tracking where it currently goes, setting meaningful goals, and choosing a system that fits your personality, you can build a roadmap to financial freedom. Remember to give yourself grace as you learn, and adjust the plan until it feels natural.