High-Yield Savings Accounts (HYSAs) vs. Traditional Banks: Stop Letting Your Money Rot

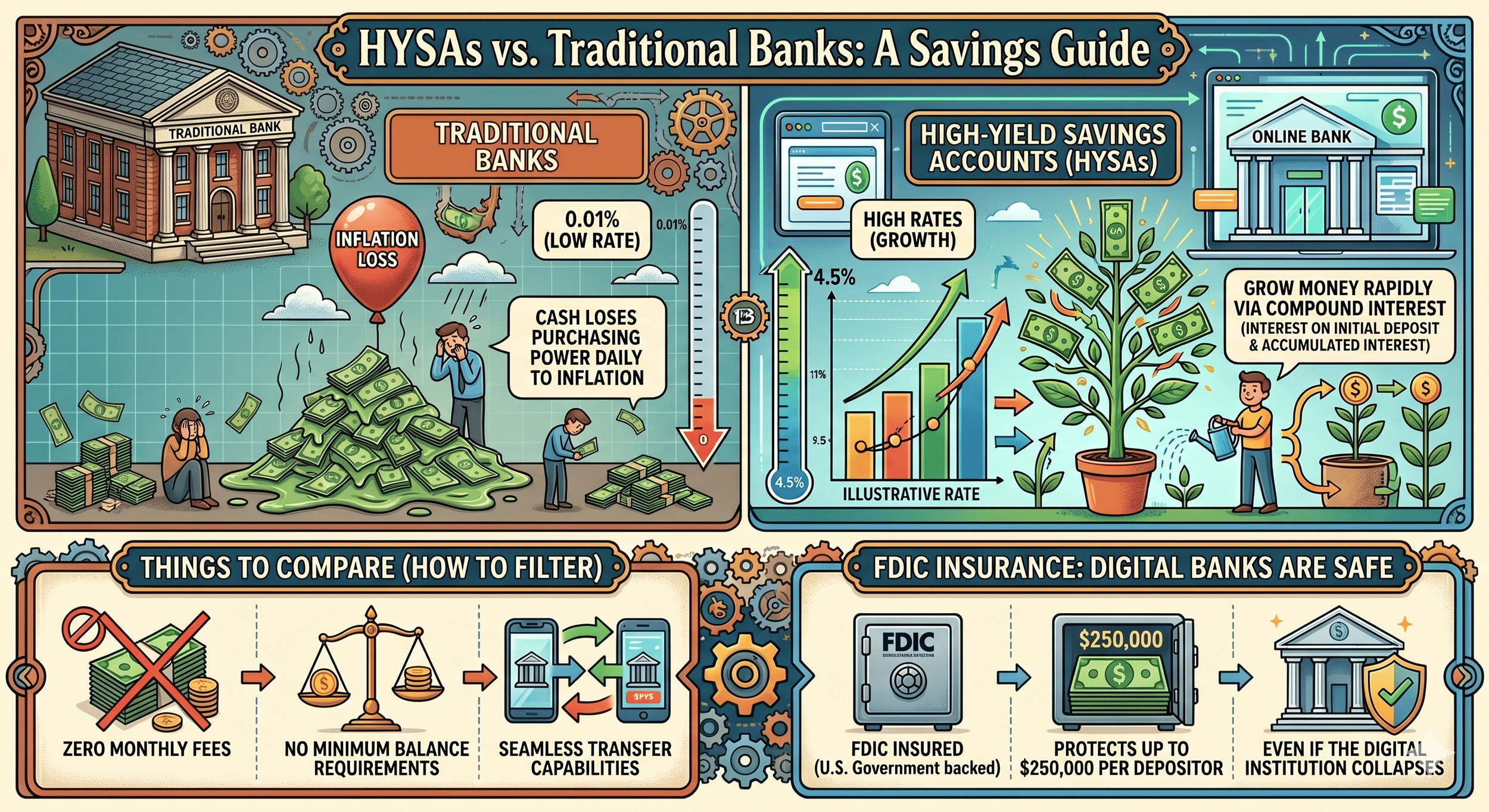

Keeping your hard-earned money in a traditional brick-and-mortar bank feels safe, but it might actually be losing you value every single day. Most big-name financial institutions offer a measly 0.01% interest rate on standard savings accounts. In an economy where the cost of goods and services steadily rises, leaving your cash in these accounts means your purchasing power (the amount of things your money can actually buy) is actively shrinking. Fortunately, there is an easy way to protect your money without risking it in the stock market.

The Magic of Compound Interest in an HYSA

The solution to the low-interest trap is moving your cash into an alternative account designed to maximize your earnings. A High-Yield Savings Account (or HYSA) is a specific type of savings account, typically offered by online-only banks, that pays an interest rate significantly higher than the national legacy bank average.

The primary engine behind these accounts is interest acceleration. Compound interest is the financial process where you earn interest on your initial deposit plus all the accumulated interest from previous periods. Traditional banks compound your interest too, but at 0.01%, the math is depressing.

To see the difference, consider a scenario where you store $10,000 of your savings:

At a traditional bank offering a 0.01% interest rate, your $10,000 will earn a tragic $1 after a full year.

In a High-Yield Savings Account offering a 4.5% interest rate, that exact same $10,000 will earn roughly $450 in the first year alone.

Over five or ten years, compound interest turns that initial bump into a massive snowball of passive growth, all for simply choosing a different place to store your cash.

Are Online Banks Safe? Understanding FDIC Insurance

The main reason people hesitate to switch to an HYSA is that these accounts are usually offered by digital banks without physical, brick-and-mortar branches. It is completely natural to wonder if your money is safe if you cannot walk into a building to talk to a teller.

Fortunately, online banks are bound by the exact same strict federal laws as traditional street-corner banks. The gold standard of banking safety is federal backing. Federal Deposit Insurance Corporation (FDIC) insurance is a government-backed program that protects your deposited cash up to $250,000 per depositor, per insured bank, in the unlikely event that a financial institution collapses.

As long as you verify that the digital bank is a member of the FDIC, your money is just as secure online as it would be in a giant vault downtown.

How to Pick the Best Account and Avoid Hidden Fees

Switching to an HYSA is simple, but you need to read the fine print to ensure a bank is not eroding your earnings with hidden hooks. When you are shopping around for the right account, use this checklist to filter out the bad options:

Zero Monthly Fees: Avoid any account that charges a monthly maintenance fee. Your savings account should make you money, not cost you money.

No Minimum Balance Requirements: Some banks pull a bait-and-switch where they only offer their highest interest rate if you maintain a massive balance, like $5,000 or $10,000. Look for banks that offer their peak rate on all balances starting at $0.

Seamless Transfer Capabilities: Your money is useless if you cannot access it. Ensure the online bank links easily with your current checking account and allows for fast electronic transfers when you need your cash.

Summary

Leaving your emergency fund or short-term savings in a traditional bank account yielding 0.01% is essentially handing free money back to a multi-billion-dollar corporation. By opening a federally protected High-Yield Savings Account, you put the math of compound interest to work for you safely. It requires minimal effort to set up, protects your money from inflation, and ensures your financial safety net is actively growing every single month.