The Art of Paying Yourself First

Most people approach saving money with the best intentions but the wrong strategy. They wait until the end of the month to see what is left over in their checking account, promising themselves they will deposit that remaining amount into a savings goal. Unfortunately, this backward approach rarely works because human psychology and modern consumer culture are designed to drain unallocated cash. To successfully build long-term wealth, you must completely reverse your financial order of operations and prioritize your future over temporary desires.

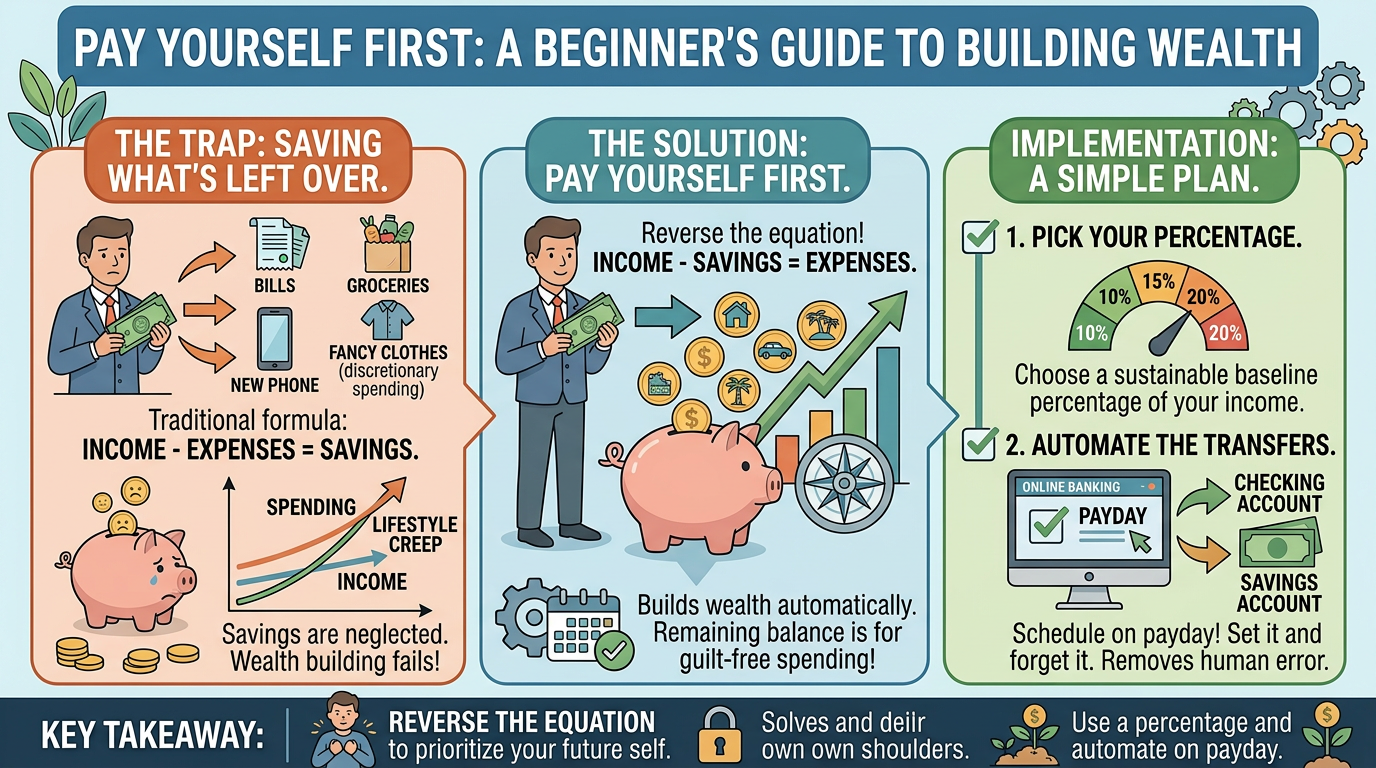

The Flawed Traditional Formula

The standard approach to personal finance relies on a deeply flawed mathematical equation: Income - Spending = Savings. Under this model, you receive your paycheck, pay your bills, buy groceries, spend money on entertainment, and then try to save whatever survives. The problem with this method is that it treats saving as an afterthought. Human beings possess a finite amount of daily willpower, and constantly fighting the urge to spend money over a thirty-day cycle inevitably leads to decision fatigue.

Furthermore, this formula leaves you highly vulnerable to lifestyle creep, which is the gradual increase of your discretionary spending as your income rises. When cash sits idly in a checking account, your brain perceives it as available for consumption. When saving is positioned at the very end of the financial food chain, it almost always gets starved out by immediate, short-term desires.

The Wealth-Building Formula

To break the cycle of living paycheck to paycheck, you must adopt a proactive mathematical model: Income - Savings = Spending. This strategy requires a total mental shift known as paying yourself first, which is the practice of routing a predetermined portion of your income into savings or investment accounts the exact moment you get paid, before paying any bills or buying groceries. By moving your savings goal to the absolute front of the line, you treat your future self as your most important monthly financial obligation.

This flips the psychological script entirely. Instead of feeling restricted by a budget, you are left with a pool of guilt-free spending money. Whatever cash remains in your checking account after your savings have been removed is yours to use completely. You no longer have to worry about whether a dinner out or a new pair of shoes will ruin your financial goals because your savings have already been secured.

Putting the Strategy into Practice

Transitioning to this new financial habit does not require a massive income, but it does require tactical execution. You can easily integrate this mindset into your daily life by using a few practical steps:

Determine a sustainable baseline percentage, such as ten percent of your take-home pay, to dedicate to your future goals immediately.

Set up your payroll system or banking app to automatically transfer that specific dollar amount to your high-yield savings account on payday.

Adjust your remaining monthly expenses to fit comfortably within the leftover balance, forcing yourself to live efficiently on what remains.

Summary

The art of paying yourself first completely removes human error and willpower from the financial equation. Moving from a model where saving is an afterthought to a wealth-building system where saving is the priority guarantees that your net worth grows consistently. It reframes your relationship with money, transforming saving from an act of painful deprivation into an automated foundation for true financial freedom.