How the 2008 Housing Bubble Popped the Global Economy

In the mid-2000s, the global financial system looked invincible. The stock market was roaring, home prices were soaring, and Wall Street banks were posting record profits year after year in what felt like a perpetual wealth machine. Then, almost overnight, the machine shattered. The 2008 Global Financial Crisis, often called the GFC, became the worst economic meltdown since the Great Depression, wiping out trillions of dollars in wealth, destroying millions of jobs, and forcing governments to step in with historic bailouts. Understanding why this disaster happened is more than just a history lesson; the scars of 2008 completely rewrote the rules of the modern financial system.

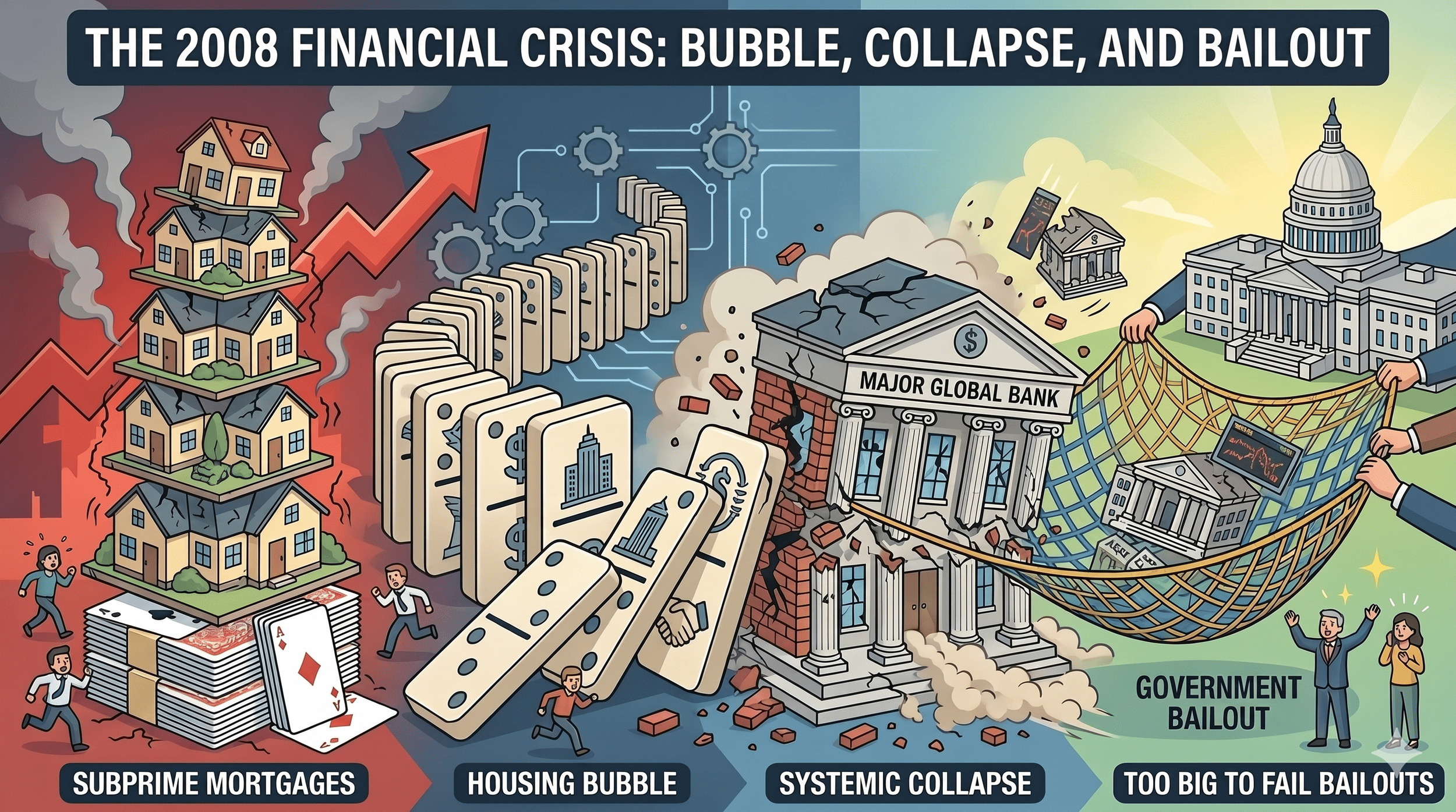

Why It Happened: The Toxic Housing Bubble

The root cause of the crisis can be summed up in two words: housing and greed. It started with a massive push to increase homeownership, which led mortgage lenders to begin offering subprime mortgages. A subprime mortgage is a home loan given to a high-risk borrower with a weak credit history or low income. Lenders did not care if these borrowers could actually afford the loans long-term. They often used teaser rates that started very low but exploded into massive, unaffordable payments a few years down the road.

Lenders were reckless because they had no intention of holding onto these risky loans. Instead, they sold them to Wall Street investment banks. Wall Street took thousands of these individual home loans, bundled them together into a single financial product, and sold pieces of that bundle to investors worldwide. These bundles were called Mortgage-Backed Securities or MBS. To make things worse, the major credit rating agencies rubber-stamped these bundles with elite, triple-A ratings, marking them as safe as government bonds. In reality, they were financial time bombs built on a foundation of unpaid debt.

The Collapse: The Domino Effect

Around 2006, the housing bubble popped as home prices stopped rising and began to plummet. Suddenly, millions of subprime borrowers saw their monthly mortgage payments skyrocket just as their homes became worth less than the money they owed, causing defaults to spread like wildfire. Because those mortgage-backed securities were scattered across the global financial system, no one knew which banks were holding the toxic losses, and widespread panic set in.

This collapse triggered a devastating corporate domino effect across the financial sector:

Banks stopped lending money to each other because they were terrified the other bank would go bankrupt tomorrow, a crisis of asset liquidity known as a credit crunch.

In September 2008, Lehman Brothers, a massive and legendary Wall Street investment bank, officially collapsed into bankruptcy due to its toxic exposure.

The failure of Lehman Brothers triggered a global chain reaction, proving that even the largest firms were vulnerable and bringing down or endangering other giant financial institutions that were deeply interconnected through complex financial contracts.

With major corporations failing, the stock market crashed, businesses could no longer get routine loans to pay their workers, and the entire global economy ground to a terrifying halt.

The Crucial Lessons We Learned

The world economy was eventually saved from total collapse through unprecedented government intervention, but the disaster taught us several painful lessons. First, we learned the danger of institutions that are Too Big to Fail. This is a phrase used to describe a financial institution so large and interconnected that its bankruptcy would trigger the collapse of the entire economic system. Because their individual failures would destroy the broader economy, governments were forced to use taxpayer money to bail these massive companies out, a move that sparked widespread public anger.

Second, we learned that transparency is non-negotiable. Wall Street had created a shadow banking system using incredibly complex derivatives that even top executives did not fully understand. Regulators realized they could no longer allow trillions of dollars in financial contracts to trade in the dark without government oversight. Third, banks need bigger safety cushions. Before the crisis, banks were operating with dangerously low amounts of actual cash on hand, causing them to instantly run out of money when the crisis hit.

Why It Is Important Today

The 2008 crisis fundamentally altered the world we live in today, completely changing how central banks operate. To save the economy, central banks began printing trillions of dollars to buy up assets, a massive experiment that permanently altered global interest rates and inflation dynamics.

It also resulted in the creation of strict new laws, such as the Dodd-Frank Act in the United States. These laws legally force banks to hold massive cash reserves, undergo regular financial stress tests, and limit their ability to make wild, speculative bets with everyday consumer deposits. Ultimately, the crisis shattered public trust in financial institutions and experts. The economic pain felt by regular families while Wall Street banks received government lifelines created political and social ripples that the world is still navigating today.

Summary

The 2008 Global Financial Crisis was caused by a combination of reckless subprime lending, complex and hidden Wall Street derivatives, and a blind belief that housing prices would never fall. When the housing bubble burst, it triggered a corporate domino effect that froze global credit, caused the historic bankruptcy of Lehman Brothers, and brought down other giant financial institutions. The crisis taught the world that banks must be strictly regulated, heavily capitalized, and transparent, proving that when Wall Street takes unmanaged risks, everyday citizens end up paying the price.