The Great Depression: A Comprehensive Overview

The Great Depression stands as the most severe and prolonged economic downturn in the history of the industrialized world, lasting from the fateful stock market crash of 1929 until the onset of World War II in 1939. Originating in the United States, the economic catastrophe rapidly infected the global economy, causing cascading failures across financial, industrial, and agricultural sectors worldwide. It was an era defined by unprecedented unemployment, widespread poverty, and a profound crisis of confidence in capitalist institutions. During this decade, the gross domestic product of the world plummeted by an estimated 15%, a staggering figure compared to modern recessions. The widespread devastation compelled governments to radically rethink their roles in economic management and social welfare, fundamentally altering the relationship between the state and its citizens. Understanding this dark chapter is essential, as the policies, institutions, and economic philosophies forged in its fires continue to shape the modern world.

What Caused the Collapse

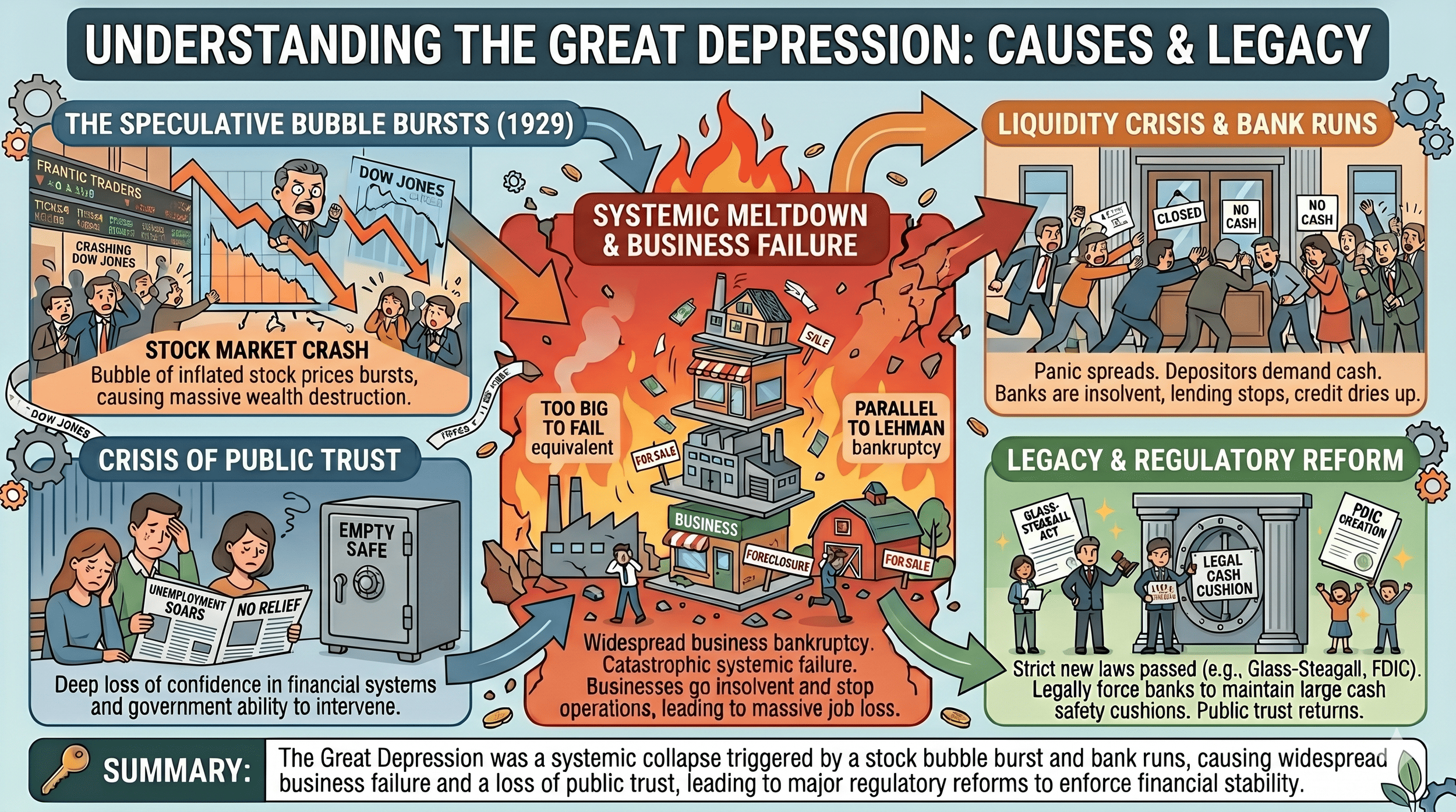

While the infamous stock market crash of October 1929, known as "Black Tuesday," is often cited as the starting point, it was merely the spark that ignited a volatile mixture of underlying economic weaknesses. Throughout the 1920s, a period of perceived boundless prosperity, systemic flaws were quietly mounting. One of the primary causes was the vast unequal distribution of wealth; the working class lacked the purchasing power to absorb the massive output of highly efficient, newly industrialized factories. This led to dangerous overproduction in both manufacturing and agriculture. Farmers, having expanded heavily during World War I, found themselves producing surplus crops that drove prices down to unsustainable levels, leading to mass rural bankruptcies long before the urban crash.

The banking system was equally fragile. Comprised of thousands of small, uninsured, and under-regulated independent banks, the system was highly susceptible to panics. When the stock market collapsed, wiping out millions of investors, a crisis of confidence ensued. Depositors rushed to withdraw their funds in "bank runs," forcing institutions to call in loans and sell assets at fire-sale prices, ultimately causing thousands of banks to fail and evaporating the life savings of countless families. Furthermore, international policies severely exacerbated the crisis. In an attempt to protect domestic industries, the United States enacted the Smoot-Hawley Tariff in 1930. This deeply protectionist measure sparked retaliatory tariffs from other nations, collapsing global trade by more than 60% and ensuring the depression became a worldwide phenomenon.

The Global and Domestic Impact

The human toll of the Great Depression was staggering in its scale and severity. In the United States, unemployment peaked at nearly 25% by 1933, leaving roughly 15 million Americans without work or reliable income. Industrial production fell by half, and wages for those fortunate enough to retain employment plummeted. Soup kitchens, breadlines, and massive encampments of homeless individuals, sarcastically dubbed "Hoovervilles" after President Herbert Hoover, became ubiquitous fixtures in cities across the nation. Families were fractured as desperate individuals scoured the country by rail in search of seasonal work.

In America’s heartland, the economic misery was compounded by an ecological disaster known as the Dust Bowl. Years of severe drought, combined with aggressive and unsustainable farming practices that had stripped the Great Plains of its native, moisture-retaining grasses, resulted in massive dust storms. These "black blizzards" choked livestock, destroyed millions of acres of farmland, and forced a massive migration of destitute farmers, often referred to as "Okies", westward toward California in a desperate search for survival. Internationally, the depression destabilized fragile post-World War I democracies, particularly in Europe. The economic desperation in nations like Germany and Italy created fertile ground for the rise of totalitarian and fascist regimes, ultimately paving the way for the Second World War.

Government Response and Restructuring

The initial response by the U.S. government, under President Herbert Hoover, relied heavily on volunteerism and the belief that the economy would naturally self-correct without direct federal intervention. However, as conditions worsened, it became clear that unprecedented action was required. The election of Franklin D. Roosevelt in 1932 marked a seismic shift in governance. Roosevelt immediately launched the "New Deal," a sweeping and experimental series of programs, public work projects, financial reforms, and regulations centered around the "Three Rs": Relief for the unemployed, Recovery of the economy to normal levels, and Reform of the financial system to prevent a repeat depression.

To provide immediate relief, the government created agencies like the Civilian Conservation Corps (CCC) and the Works Progress Administration (WPA), which employed millions of men to build infrastructure, plant trees, and construct public buildings. To stabilize agriculture, the Agricultural Adjustment Act (AAA) paid farmers to reduce crop production, successfully raising prices. Most significantly, the government enacted profound structural reforms. The Glass-Steagall Act separated commercial and investment banking, while the creation of the Federal Deposit Insurance Corporation (FDIC) insured bank deposits, instantly ending the epidemic of bank runs. Additionally, the Securities and Exchange Commission (SEC) was established to police the stock market and enforce transparency.

Why It Is Important

The Great Depression is historically significant because it permanently transformed the landscape of modern governance, economics, and society. Prior to the 1930s, the prevailing economic orthodoxy was "laissez-faire," which is the idea that governments should not interfere in the free market. The catastrophe proved that markets are not always self-correcting and that periods of deep contraction require active state intervention. This paradigm shift gave rise to Keynesian economics, the theory that governments must use fiscal and monetary policy to stimulate demand during economic downturns.

Furthermore, the crisis established the modern social safety net. The passage of the Social Security Act in 1935 introduced unemployment insurance, old-age pensions, and welfare assistance for the disabled and impoverished, fundamentally redefining the government's obligation to its vulnerable citizens. Globally, the era demonstrated how economic instability can rapidly translate into political extremism and conflict, serving as a permanent warning about the fragility of global peace when economic foundations crumble.

Enduring Lessons Learned

The hardships of the 1930s yielded crucial lessons that continue to guide modern economic policy. Among the most critical takeaways are:

The Necessity of Central Bank Intervention: The Federal Reserve's initial failure to inject liquidity into the failing banking system worsened the crash. Today, central banks recognize the necessity of acting as the lender of last resort during financial panics.

The Danger of Protectionism: The catastrophic failure of the Smoot-Hawley Tariff illustrated that engaging in aggressive trade wars during a downturn only deepens global recessions. Cooperative international trade policies are vital for economic health.

The Importance of Financial Regulation: Unchecked speculation and lack of transparency in financial markets inevitably lead to ruin. Institutions like the SEC and the FDIC are vital for maintaining public trust and ensuring that reckless gambling does not endanger the broader economy.

The Role of Fiscal Stimulus: When private sector demand collapses, the government must step in to spend, invest, and create jobs to break the cycle of deflation and unemployment.

Summary

The Great Depression was a transformative global crisis that tested the very foundations of democratic capitalism. Triggered by a toxic combination of extreme wealth inequality, an overleveraged and under-regulated financial system, and protectionist trade policies, the decade-long struggle brought unimaginable hardship to millions across the globe. However, out of this profound suffering emerged a modernized state equipped with essential safeguards. By abandoning strict laissez-faire policies in favor of active economic management, social safety nets, and rigorous financial oversight, society forged the tools necessary to mitigate future crises. The legacy of the 1930s serves as an enduring reminder of the interconnectedness of global economies and the indispensable role of responsible governance in maintaining stability and protecting human welfare.